A lot can happen in 10 years. Elections, World Cups, various government regimes, the Olympics, and Arrested Development have all come and gone several times in a span of a decade. But how much do companies change? That is the question we are attempting to answer today.

Data disclaimer: we are using sub-industry aggregated data based on an equal-weighting of sub-industry constituents in the MSCI World. All of the data is "as-reported". We have excluded financial companies for the same reason that Eugene Fama and Ken French, and many others, do (i.e. high leverage that is normal for financial firm is not normal for non-financial firms).

The preliminary answer to our questions is this: company fundamentals have changed and mostly for the better. In general, corporations have improved their profit margins, have slightly less geared balance sheets, have increased their cash flow and are distributing a greater percentage of their cash flow back to investors via dividends and share repurchases.

We all know that based on traditional measures corporate profit margins are historically high. There are many who make the case that profits are mean-reverting while there are others who argue that the popular way of measuring profit margins (corporate profits as a % of GDP in Chart 1) are mismatching "global profits" to "domestic" GDP and thus, may not ever mean-revert to pre-2000 norms.

Chart 1

Analysing our bottom up data, we find is that gross margins and net margins have both increased in the past decade. Median gross margins have increased by 23% since 2003 and the increase has been fairly steady (Figure 2). Median net margins have nearly double during that time as well (Figure 3) but with more year to year variability than gross margins. The most disappointing data point that we came across in our work was the drop in the year-over-year sales growth rate (Figure 4). From 2004-2008, sales grew by at least 10% each year. Since the Great Recession sales growth has slowed by about 50%. Perhaps, this is why we are witnessing such a record high valuation premium being placed on sales right now (Chart 2).

Figure 2

Figure 3

Figure 4

Chart 2

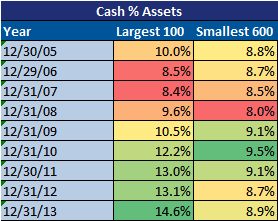

Moving on to the balance sheet. we see that long-term debt as a % of capital has slightly increased over the past decade (Figure 5). Cash as a % of capital has also increased (Figure 6) which in turn has actually brought down net debt as a % of capital (Figure 7). Encouragingly, return on invested capital has moved back to levels seen pre-recession (Figure 8) and contrary to what you may have read elsewhere, corporations are still investing and have held traditional tangible capital expenditures and investments very steady (Figure 9 and 10).

Figure 5

Figure 6

Figure 7

Figure 8

Figure 9

Figure 10

Cash flow generation has also been on the rise. Median FCF as a % of sales has increased by 42% since 2003 (Figure 11). The good news for investors is that management is giving back more of that cash flow than before by increasing both dividends and share repurchases as a % of operating cash flow significantly. Median dividends as a % of operating cash flow has increased by 127% (Figure 12) and median share repurchases as a % of operating cash flow has increased by 186% (Figure 13).

Figure 11

Figure 12

Figure 13

Overall, even with the Great Recession and the global fianncial crisis, corporate fundamentals have more than weathered the storm and have actually improved over the past 10 years. Have they improved enough to justify the

record valuations levels that we are currently experiecing? That is a question left to answer for another day.

(source: Gavekal Capital)