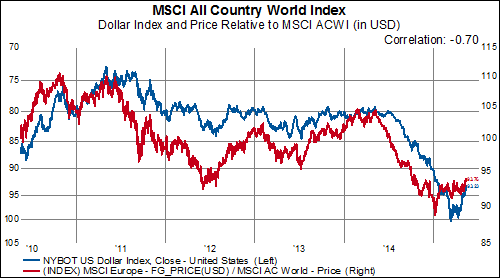

While we entered 2015 with the Federal Reserve talking confidently about lift-off and how many rate increases there would be by the end of the year, the markets didn't seem to buy it. As weak economic data began to surface, the Fed seemed to quietly backtrack first on the date of lift-off and then on the trajectory of the expected hiking cycle.

We always believe that Fed actions speak louder than words, and for this reason we measure high frequency monetary movements. In the last couple months, the Fed seems to have arrested the decline in its balance sheet that began in 2014. This has had positive impacts on liquidity in the banking system. In the first chart, we show the three month change in total Fed assets. The latest reading of $4.5 billion is in contract to the negative readings we have seen most of the year.

In the second chart, we show the relationship between Fed assets and commercial bank liquidity. Movements in commercial bank non-borrowed reserves mirror movements in Fed assets, but with more volatility. So, in the last few months, as the contraction in Fed assets has ceased and turned positive, commercial bank liquidity experienced a much more dramatic swing.

This reversal in liquidity trends have fueled the latest stock market movements. In the next chart, we show the same three month change in non-borrowed reserves as shown above, but this time we overlay the percent of stocks in the MSCI World index that are above their 200-day moving average. Clearly liquidity trends have a big impact on equity movements.

Will recent favorable liquidity trends be enough to propel stocks out of the current consolidation relative to bonds? In the chart below, we show the total return of the S&P 500 compared to the total return of the JP Morgan 10 Year Government Bonds Index.

Two economic readings have us skeptical. First, in the chart below, we show the S&P 500 compared to lumber prices. Lumber is a good proxy for the strength of the housing market and, in turn, the housing market is a good proxy for the strength of the economy. The plunge in lumber prices would suggest investors are skeptical on the strength of the housing market and, in turn, the economy.

Next, the Citi Economic Surprise Index keeps deteriorating. The current reading of -73 is the weakest since the fall of 2011... and a 20% correction in stock prices. We keep a one year running total of the Citi Economic Surprise Index, and its keeps falling. Another month of weak data, and it is likely our indicator takes out the lows last seen in October 2011.

If the Fed has quietly decided to not only abandon any prospect of rate increases, but begin expanding its balance sheet again (in some stealth QE), stocks probably do propel out the year long relative strength consolidation with bonds. But, if not, then stock managers should be particularly attuned to monetary movements and the economic mirage in the US. Our simple model of the change in Fed asset compared to the total return of stocks vs. bonds, suggests the potential for significant bond outperformance if the Fed sticks to its plan of a 2015 lift-off.