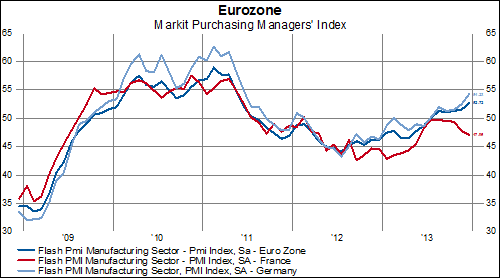

Important survey data out of Europe today points to a growing disparity between the region's two largest economies. While the Eurozone and Germany both surpassed consensus estimates, France's flash PMI came in at a disappointing 47.1 (versus expectations for a small rise to 49.1 from last month's 48.4):

Meanwhile, business confidence has stalled...

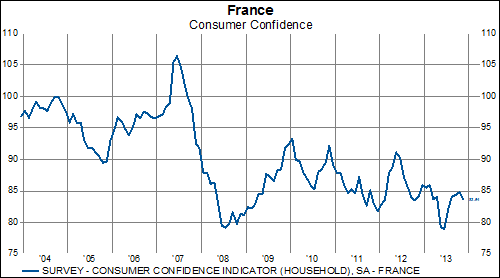

Consumer confidence isn't showing much life...

Unemployment continues to climb...

While labor cost increases have dramatically outpaced those of Germany over the last two decades...

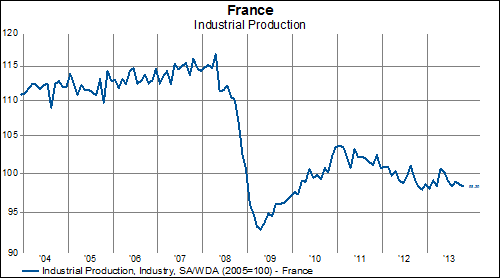

Industrial production remains well below pre-recession levels...

Exports are falling in the face of a rising euro...

Debt as a percent of GDP shows no sign of slowing...

And the CAC lags both the German and Swiss exchanges year to date-- not to mention stock markets in the GIPSIs...

But, hey-- inflation doesn't appear to be much of a problem these days!