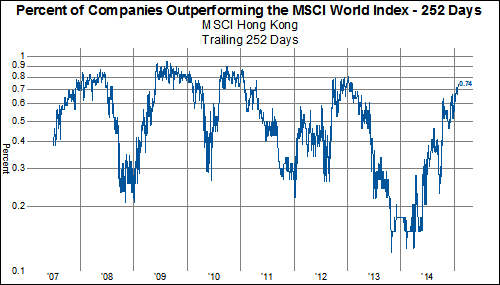

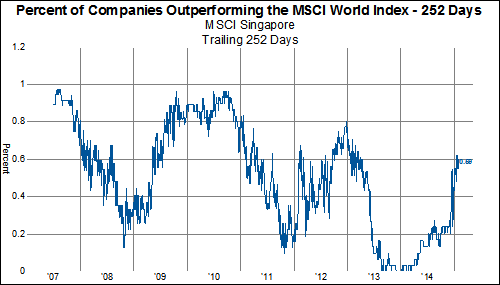

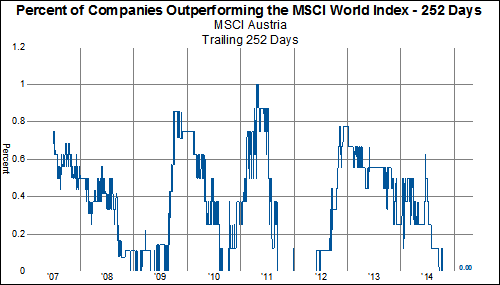

Looking across the global equity markets, it is clear that an asset allocation approach based on sector exposures has worked better than any geographic allocation. In particular, an overweight allocation to the health care sector would have benefited portfolios tremendously. With oil collapsing, the USD soaring and the ECB on the cusp of a massive asset purchase, investors are probably wondering whether it is time to rotate out of the healthcare sector, in pursuit of higher beta companies. Not yet!

In the charts below, we show the YTD performance by sector of various geographies. First, we'll show the aggregate MSCI Developed World and the MSCI Emerging Markets.

MSCI Developed World

MSCI Emerging Markets

MSCI Emerging Markets

While the health care sector is not the top performing sector in the EM, it has still performed better than any developed market sector, up 5.16% YTD.

Next, let's look at the components of the developed world, staring with North America, then Asia and then Europe.

MSCI North America

MSCI Asia-Pacific

MSCI Asia-Pacific

MSCI Europe

MSCI Europe

Now, we turn our attention to the emerging markets. We'll start with EM Asia, then show EM EMEA and EM Latin America.

MSCI EM Asia

MSCI EM EMEA

MSCI EM EMEA

MSCI Latin America

MSCI Latin America

With the sole exception of Latin America, health care is the first or second best performing sector, with positive performance in all geographies. Investors with lots of health care exposure are experiencing a continuous drip feed of alpha.